Introduction

Every year, CU produces an audited financial report with a vast amount of information that is very important to a number of constituencies: rating agencies, the State of Colorado, federal funding agencies, the Board of Regents, and the public. However ... providing a vast amount of information is not the same as providing easily understandable information. So the Office of University Controller decided to present the data in easy-to-understand language and charts.

You could call this ‘financial statements made easy' ... or ... ‘financial statements for the non-accountant' ... or ... ‘the ABCs of CU's annual financial report'. Whatever you call it, this is our commitment to helping interested people better understand the University of Colorado's financial position. Through this website, you will see where CU holds its resources, what the claims against those resources are, and what's left over in the end.

Along the way, we'll tell you where the University gets its money and how it spends it - in the short term and over the long haul. All of the numbers in this website are taken from CU's audited financial statements.

A few definitions

Basic Terms/Concepts

Accounts Receivable - assets due the University, primarily the receivables due from students (for tuition and fees); from federal, state, and private sponsors (for research); and from patients (treated by School of Medicine faculty)

Accrued Expenses - expenses reported in the period in which they occur but for which payment is made in a subsequent period. The vast majority of the University's accrued expenses are salaries and benefits earned but not paid as of the end of the fiscal year due to the State's pay date shift (shifting the final pay date for all State employees from June 30 to July 1 of each year).

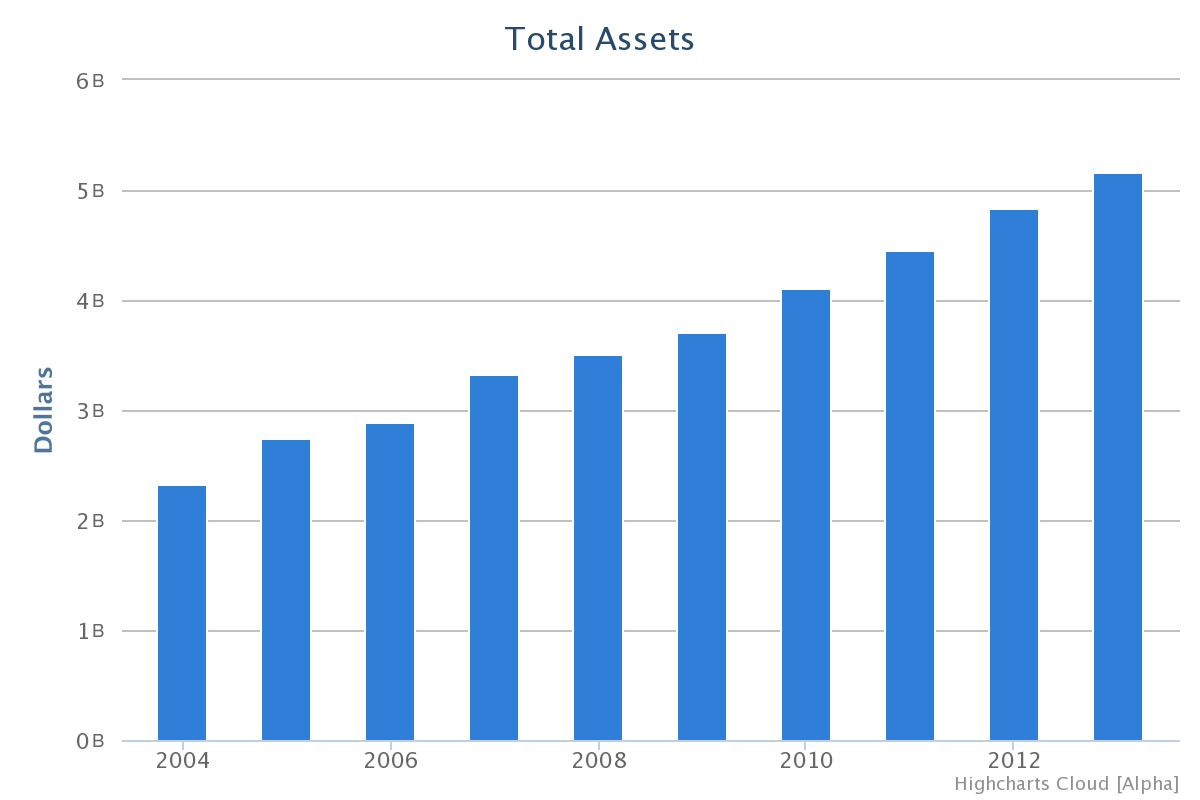

Assets - resources held by the University

Capital Assets - the University's buildings, land, equipment, library books, and other tangible assets that are used to teach students, conduct research, and handle daily operations

Compensated Absences - the dollar value of paid time off earned but not yet used by University employees (sick leave, personal leave) plus employer-related payroll taxes

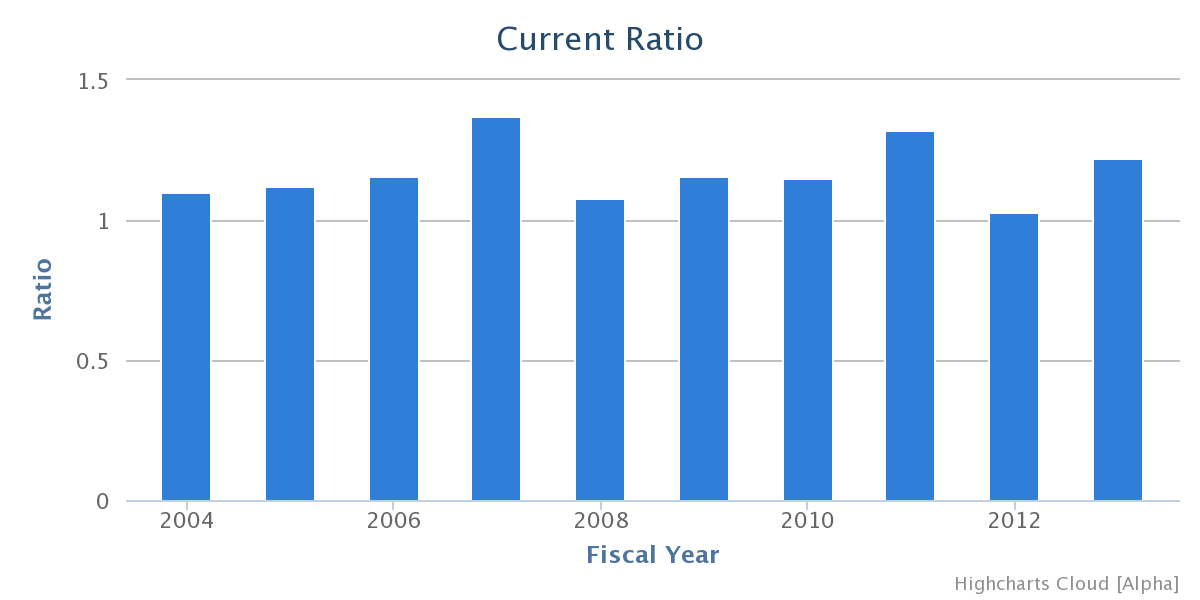

Current Assets - assets expected to be used within one year (like inventories) or that will convert to cash within one year (like current investments and current accounts receivable)

Current Liabilities - liabilities that will be paid within one year

Deferred Outflows - a consumption of resources applicable to a future reporting period (these are essentially assets)

Liabilities - claims against the University's resources (assets)

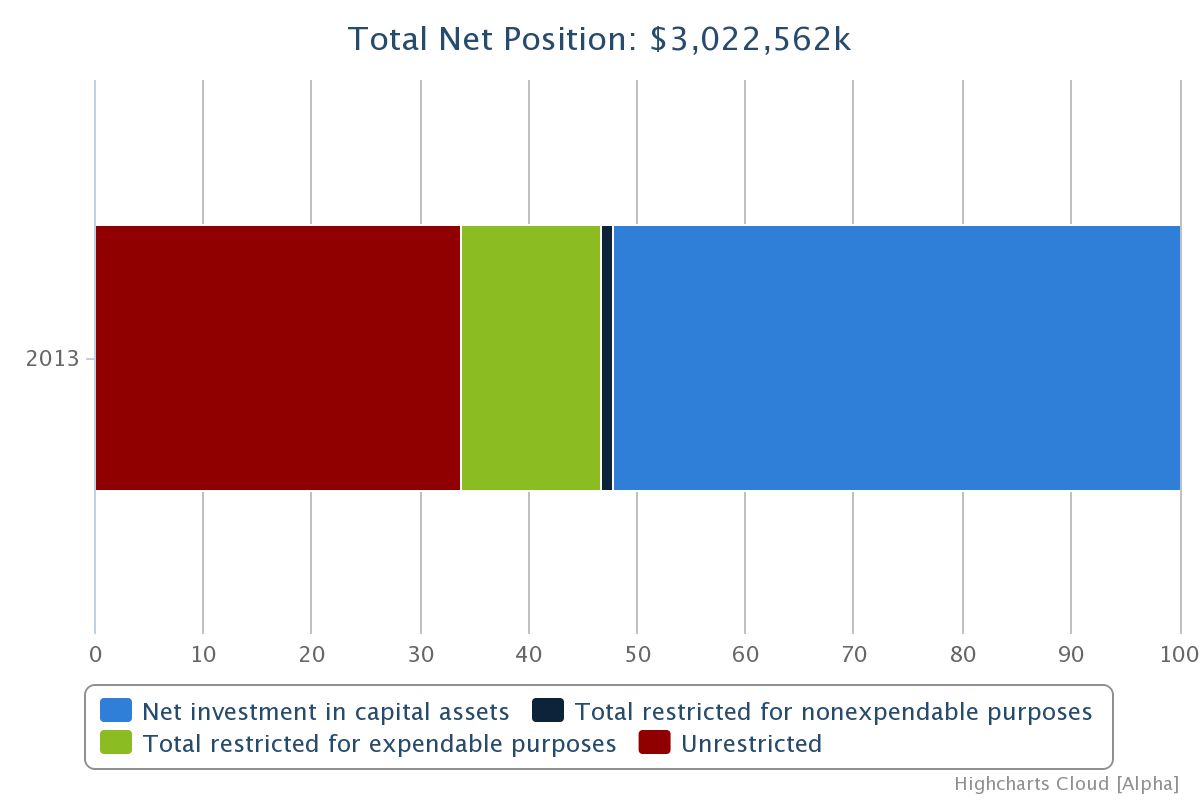

Net Position - assets plus deferred outflows less liabilities (essentially, the difference between resources and claims against those resources). Net position can either be positive (usually a good thing) or negative (probably a bad thing).

Noncurrent Assets - assets that exceed the one-year time frame

Noncurrent Liabilities - claims that exceed the one-year time frame

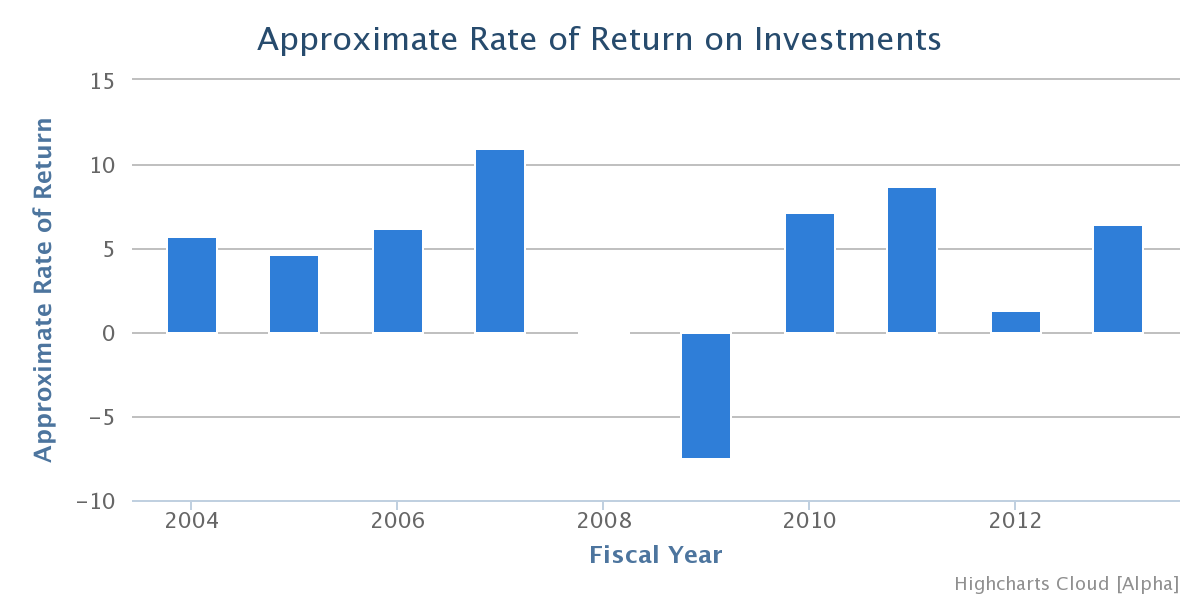

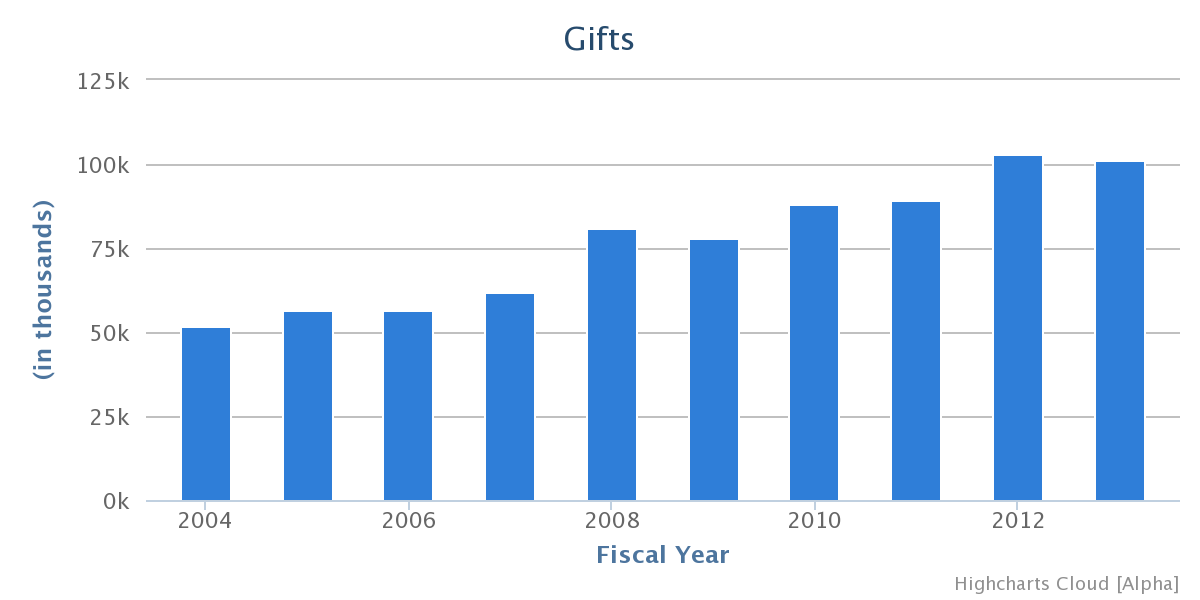

Nonoperating Revenues and Expenses - those amounts that are not directly related to the University's primary missions but are still important drivers of its financial results (major nonoperating revenues are the federal Pell Grant, gifts, and investment income ... major nonoperating expenses are investment losses and interest expense on the University's outstanding debt)

OPEB (other postemployment benefits) - health and other benefits provided to individuals after their University employment has ended but reported as a liability in the financial statements as the benefits are earned by the still-active employees

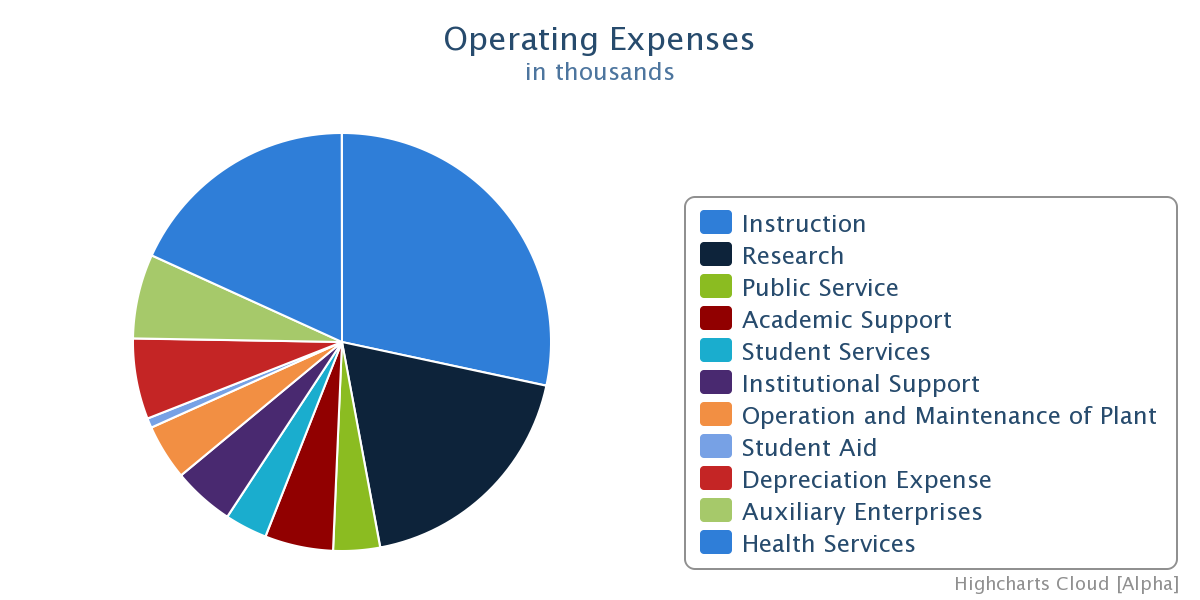

Operating Expenses - costs incurred in fulfilling the University's primary missions (classified by function, e.g., instruction, research, health services)

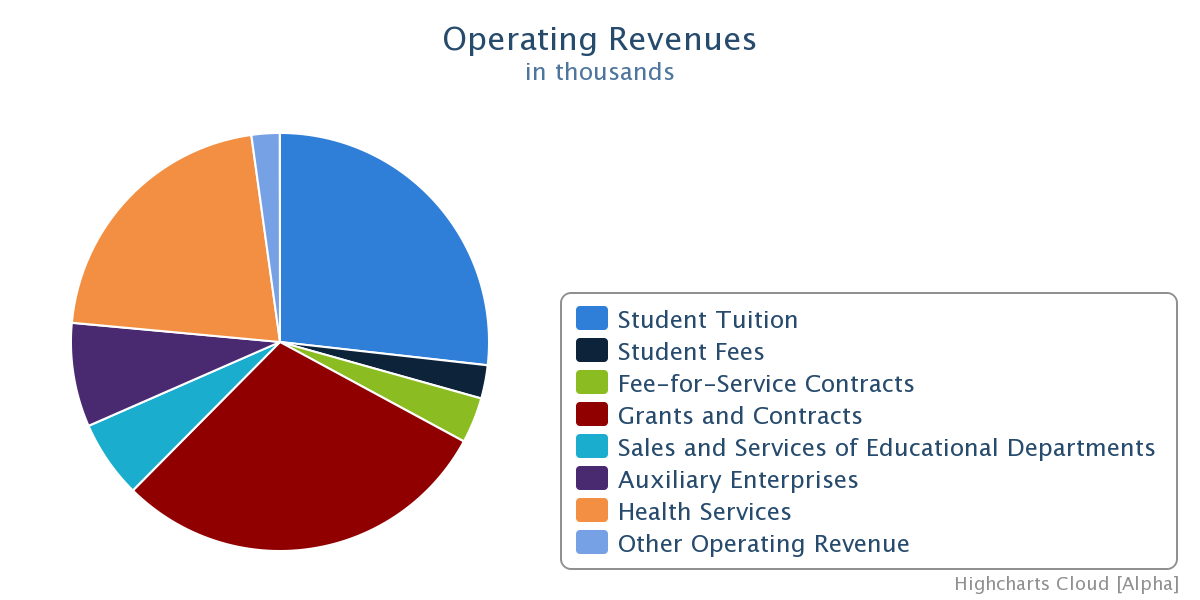

Operating Revenues - revenues (money) received from what the University does as its primary missions: teach, conduct research, auxiliary enterprises, and health services

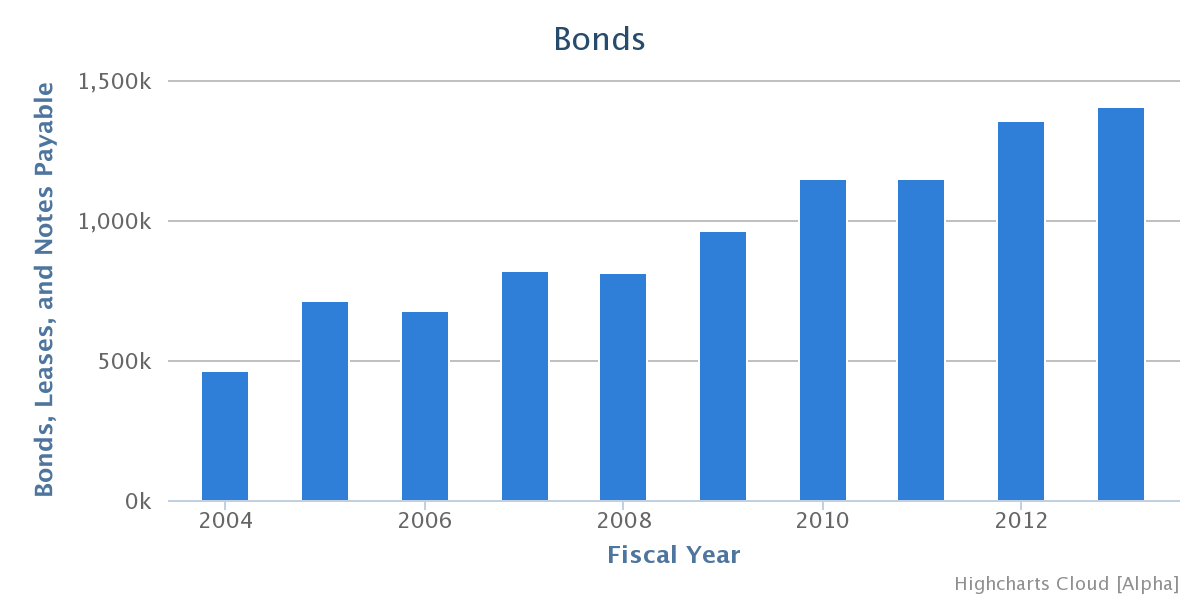

Revenue Bonds - bonds payable from revenue sources specified in the debt agreements, normally issued to fund capital improvements. Revenue sources include auxiliary services (parking, dining, housing, athletics, etc.), research services, tuition (limited to ten percent of the University's total), capital student fees, and indirect cost recoveries (funds received, typically from the federal government, to pay for certain costs of managing funded research activity)

Unearned Revenue - payments for services that have come to the University in advance of the University providing those services (e.g., summer tuition and fees paid for courses that are not completed by June 30, and payment on grants and contracts prior to the research being conducted/work being performed). Unearned revenue is treated as a liability since the University has not yet performed the work (teaching, research, etc.) needed in order to “earn” that revenue.